Improved Credit Scoring and Loan Prediction

HumAIze Fintech Hackathon

Topic - Improved Credit Scoring and Loan Prediction

Team Name - Odyssey

Team Members

Aniruddha Kumar

Deekshit Kashyap

Sanika Awal

What is Our Idea?

People arent aware of credit score and how to get the loan efficiently, without getting any problems in their path, for easier approach we plan to integrate the Neural Network Expert System and create a sophisticated credit scoring and loan prediction system, with a strong loan comparison function for Banks as well as a generic User, suggesting ways to manage their risk and provide/give loan to them.

Our hybrid AI approach gives precise reliable credit judgments through integrating traditional credit data with detailed financial and utility information that has already been used by banks, which will make easier integration possible with the current system.

This system also includes a loan comparison tool that integrates and displays loans available from different banks, allowing users to choose the best rates and terms based on their credit histories.

What is Unique in our Platform?

Our Neural Network Expert System approach improves credit ratings by combining neural network precision with expert system clarity and fairness. In addition, we provide a unique loan comparison tool that offers users clear, side-by-side comparisons of loan choices from multiple banks. This makes complex financial decisions easier and increases trust.

Neural Network Expert System:

Integrates the precision of neural networks with the fairness and explainability of expert systems, ensuring accurate and transparent credit evaluations.

Loan Comparison Tool:

Provides exceptional transparency by offering users clear, side-by-side comparisons of loan options from various banks, empowering them to make informed decisions.

Enhanced Financial Decision-Making:

Simplifies complex financial choices, boosting user confidence and trust in t heir financial future.

How do we plan to impact the world ?

We are planning to empower the users as well as the banks with accurate credit scores which will be trained using the neural network frameworks and will improve the loan accessibility to a normal person based on the parameters defined.

Hence, following are the major points:

Personalised loan based on data

Risk Management to Bank using Early prediction System

Enhancing financial inclusion for normal user by providing the suggestions

Thus, building consumer trust in the fintech sector, we aim to transform the lending landscape and provide equitable financial opportunities for all.

WorkFlow

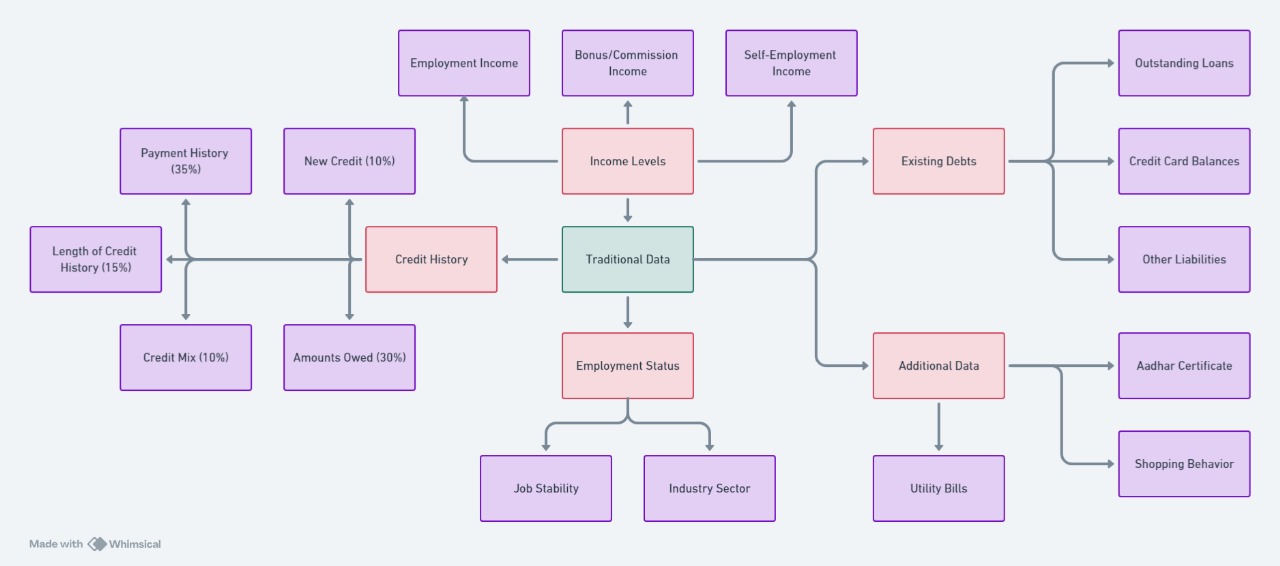

Step 1: Data Collection

Traditional Data

Credit History (35%)

Payment History: Records of timely or late payments on credit accounts, loans, and other debts.

On-time Payments: Regular, on-time payments of credit accounts.

Late Payments: Frequency and recency of late payments.

Defaults: Any instances of defaulting on loans.

Bankruptcies: Any history of bankruptcy filings.

Collections: Accounts that have been sent to collections.

Amounts Owed (30%)

Credit Utilisation Ratio: The amount of credit used compared to the total available credit. A lower ratio is preferable.

Outstanding Balances: Total amount owed across all credit accounts.

Number of Accounts with Balances: How many accounts have balances.

Proportion of Loan Balances: Balances owed on specific types of accounts, like instalment loans versus revolving accounts.

Length of Credit History (15%)

Age of Oldest Account: How long the oldest credit account has been open.

Average Age of Accounts: The average age of all credit accounts.

Age of Specific Types of Accounts: Age of different types of credit accounts, such as mortgages, credit cards, etc.

Credit Mix (10%)

Types of Credit Accounts: A mix of credit types such as credit cards, retail accounts, instalment loans, finance company accounts, and mortgage loans.

Management of Different Credit Types: How well different types of credit are managed.

New Credit (10%)

Recent Credit Inquiries: Number of hard inquiries or credit checks made by lenders.

New Credit Accounts: The number of new credit accounts opened recently.

Recent Inquiries Impact: The impact of recent inquiries on the credit score.

Time Since Recent Account Openings: How recently accounts were opened.

2. Income Levels

Employment Income: Regular wages or salary from employment.

Bonus/Commission Income: Additional earnings from bonuses or commissions.

Self-Employment Income: Earnings from business ownership or freelance work.

Other Income Sources: Income from investments, rental properties, or alimony.

3. Employment Status

Job Stability: Length of time at current job and overall employment history.

Industry Sector: The industry in which the individual is employed, as some sectors may be more stable than others.

4. Existing Debts

Outstanding Loans: Balances on personal loans, student loans, auto loans, etc.

Credit Card Balances: Current balances on credit cards.

Other Liabilities: Any other debts, such as medical bills or unpaid taxes.

5. Additional Data

Utility Bills: Payment records for utilities such as electricity, water, and gas.

Shopping Behaviour: Insights from shopping habits and transaction records.

Income Tax Returns (ITR): Detailed records of filed income tax returns.

Aadhar Certificate: Unique identification information.

Know Your Customer (KYC): Documents and information required for verifying identity.

Step 2: Data Preprocessing

Data Cleaning: Handle missing values, outliers, and inconsistencies.

Data Transformation: Normalise/standardise numerical data, encode categorical variables.

Feature Engineering: Create new features from the existing data to enhance model performance.

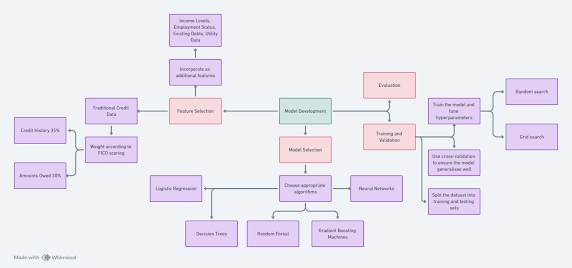

Step 3: Model Development

Feature Selection

Traditional Credit Data: Weight according to FICO scoring (e.g., Credit History 35%, Amounts Owed 30%, etc.).

Income Levels, Employment Status, Existing Debts, Utility Data: Incorporate as additional features.

Model Selection

Choose appropriate algorithms such as:

Logistic Regression

Decision Trees

Random Forest

Gradient Boosting Machines

Neural Networks

Training and Validation

Split the dataset into training and testing sets.

Use cross-validation to ensure the model generalises well.

Train the model and tune hyperparameters using grid search or random search.

Evaluation

Evaluate the model using metrics like accuracy, precision, recall, F1-score, and AUC-ROC.

Ensure model fairness and mitigate any biases.

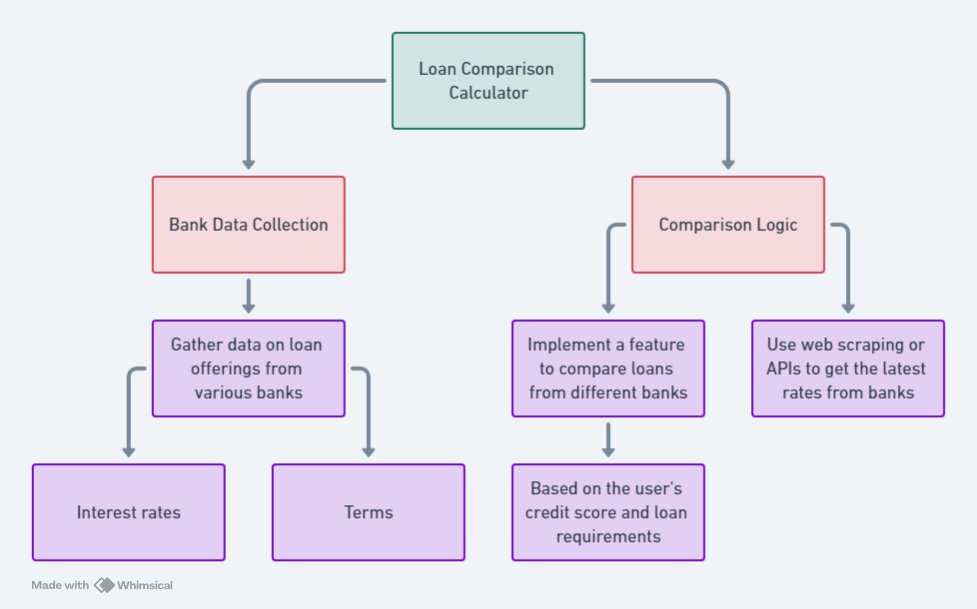

Step 4: Loan Comparison Calculator

Bank Data Collection

Gather data on loan offerings from various banks, including interest rates, loan types (mortgage, education, personal, etc.), and terms.

Comparison Logic

Implement a feature to compare loans from different banks based on the user's credit score and loan requirements.

Use web scraping or APIs to get the latest rates from banks.

Step 5: Integration and Deployment

Web Application

Streamlit Application

Neural Network Architecture

1. Input Layer:

Features: Traditional credit data, income levels, employment status, existing debts, utility data.

Data Preprocessing: Normalize numerical data, encode categorical variables.

2. Hidden Layers:

Layers: Multiple hidden layers with ReLU activation functions to capture complex patterns.

Regularization: Dropout layers to prevent overfitting.

Batch Normalization: To stabilize and speed up training.

3. Output Layer:

Credit Score Prediction: Sigmoid or softmax activation function for classification (e.g., good/bad credit).

Loan Approval Prediction: Regression output for loan amount predictions.

Expert System Architecture

1. Knowledge Base:

Rules: If-then rules derived from domain expertise and regulatory guidelines.

Inference Engine: Deductive reasoning to evaluate rules against user data.

2. Components:

Fact Database: User-specific data (e.g., credit history, income, employment).

Inference Engine: Applies rules from the knowledge base to the facts to make decisions.

Combined Architecture

1. Input Layer:

Unified Input: Consolidate inputs for both neural networks and the expert system.

Preprocessing: Data normalisation and encoding for neural networks, structured formatting for expert systems.

2. Neural Network Module:

Feature Extraction: Hidden layers extract high-level features from input data.

Interim Outputs: Provide preliminary predictions and feature embeddings.

3. Expert System Module:

Rule Application: Uses the knowledge base to apply domain-specific rules to the raw input data and interim outputs from the neural network.

Consistency Check: Ensures the decisions comply with regulatory and business rules.

4. Integration Layer:

Combination Mechanism: Merges the neural network’s probabilistic outputs with the expert system’s deterministic decisions.

Weighting Scheme: Assigns weights to the outputs from both modules to form a final decision.

5. Output Layer:

Final Predictions: Combines weighted outputs to predict credit score, loan approval probability, and recommended loan amount.

Explanations: Provides interpretability by explaining the final decision through the rules applied in the expert system.

What Technology will we use to implement the above solution?

Python, Jupyter Notebook

Libraries - Scikit-learn, matplotlib, Pandas, Seaborn

Frameworks - TensorFlow, Keras

Models - Logistic Regression, Decision Trees, Random Forest, Gradient Boosting Machines

Neural Networks and Expert System Combination to form a Rule based Expert System

Deployment - Streamlit, Docker, AWS.

Comments

Post a Comment